How Zero-Based Budgeting Can Benefit You: The Complete Guide for 2026

Zero-based budgeting gives every dollar a job before the month starts. Here is how this powerful method can transform your finances, eliminate wasteful spending, and help you build real wealth on any income.

Where did your money go last month? This is a question that most people can't honestly answer. Not quite. Would you be able to account for every dollar you spent if you had to sit down right now? Most people are unable to. And zero-based budgeting fills that gap between what you make and what you can truly account for.

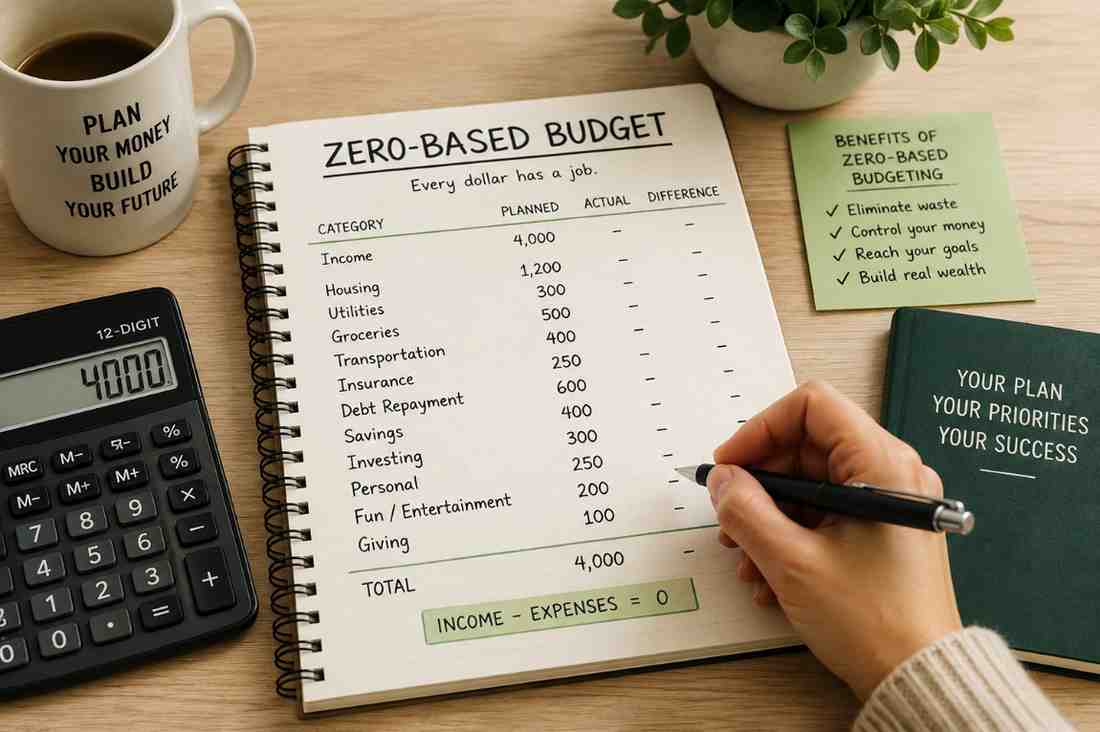

Zero-based budgeting is not complicated. The idea is brutally simple: every dollar you earn gets assigned a specific job before you spend it, so that your income minus your total allocations equals zero by the end of every month. Not zero as in broke zero as in every single dollar is working for something intentional, whether that is rent, food, savings, investments, or debt repayment. Nothing floats around unaccounted for.

What Is Zero-Based Budgeting?

Zero-based budgeting is a budgeting method in which you start each new period of budgeting from zero. Not the numbers released last month. Not from a template you created a year ago. From nothing. Instead of I spent $400 on food last month so I will just budget $400 again, you stop and say: "How much do I actually need to spend on food this month, and why?" Every single expense has to earn its place every single time.

The method was developed in the 1970s by accountant Peter Pyhrr as a corporate cost-cutting device. Big companies use it to require departments to justify their budgets from the ground up, instead of taking the previous spend as a baseline. It was later adapted for personal finance, most famously by Dave Ramsey and his EveryDollar app and Baby Steps framework. But the basic logic is the same whether you're running a company or managing a household: money doesn't go anywhere without a specific reason.

The formula looks like this: Income minus all allocated expenses equals zero. If you bring home $3,000 a month, you assign all $3,000 to specific categories rent, food, savings, transport, entertainment, investments until every dollar has a destination. When you reach zero, your budget is done. Not a dollar left unassigned, not a dollar without purpose.

Zero-Based Budgeting vs Regular Budgeting

Most people who budget at all use what is called incremental budgeting. You look at what you spent last month, make minor adjustments, and carry on. It feels efficient but it has a serious flaw: it treats your past spending as the baseline for what is normal. If you wasted $200 on things you barely remember last month, that waste automatically gets rolled into next month's plan. Nothing ever gets questioned. Nothing ever gets cut unless you are in a crisis.

| Factor | Zero-Based Budgeting | Regular Budgeting |

|---|---|---|

| Starting point | Zero every single month | Last month's numbers |

| Spending justification | Every expense must be justified | Expenses assumed necessary |

| Control level | Very high | Low to medium |

| Time required | 30 to 60 mins per month | 10 to 15 mins per month |

| Best for | Catching waste and building discipline | People who already spend carefully |

| Handles irregular income | Very well | Poorly |

| Savings treatment | Savings allocated first as a category | Savings from whatever is left over |

The last row in the table is the most important. The regular budget is usually one where people spend and then save what is left. Savings are budgeted right from the start, in a zero-based budget they are a budget line just like rent or groceries. That one change in sequence is the difference between people who always build wealth and people who always plan to save more but never do.

The 7 Real Benefits of Zero-Based Budgeting

1. You Finally Know Where Your Money Is Going

That sounds too simple to mean anything. It isn't. Most budgeting methods are reactive you scroll through your bank app at the end of the month and try to put together what happened. The opposite is true for zero-based budgeting. You pay before you plan. All categories are pre-determined, so you never have any end-of-the-month surprises. You know where every dollar went because you decided where it was going before the month even began. That clarity changes your relationship to money in ways hard to fully describe until you experience them.

2. It Exposes the Money You Are Wasting Without Realising

When you have to justify every expense from scratch every month, things you stopped noticing come back suddenly. The one you signed up for during a free trial and forgot to cancel. That magazine subscription you haven’t opened in 6 months. the premium app you pay $9.99 a month for and used twice The gym membership you keep promising yourself you’ll use next week Zero-based budgeting captures all of it because you can't carry expenses forward without actively thinking about them. Either you justify the spend or you cut it. There is no compromise.

3. Savings Become Non-Negotiable

among the most powerful mental shifts that zero-based budgeting creates is treating savings as an expense. In a zero-based budget, “savings: $300” is a line item just like “rent: $1,000.” Both get funded before you spend one dime on discretionary spending. So savings are made at the start of the month, not the end. You stop saving what's left. You begin to spend what is left after saving. It sounds small, that one change in sequence, but it is what builds real, compounding wealth over time.

4. It Works on Any Income, Including Irregular Income

Most budgeting systems are bad when income is not consistent. Freelancers, contractors, creatives, business owners and anyone with variable pay can’t keep a fixed budget when the numbers keep changing month to month. Zero-based budgeting, naturally, takes care of that. You always start from zero so you only budget the income you have. The system is self adjusting. A leaner month means a leaner budget. Better month More allocation across categories. The discipline is permanent even if the income is not.

5. Your Spending Finally Reflects Your Actual Goals

If you ask most people what their financial goals are, they will say something like building an emergency fund, or paying off debt, or investing for the future. Then look at how they actually spend and the gap between what they say is important and what they spend their money on is often huge. Zero-based budgeting bridges that gap, so each month your dollars and your goals are having a conversation. If a holiday is important enough to spend $200 on, it gets a line in the budget. If paying down a credit card balance is a priority, it gets its own allocation. If it's not in the budget it's not really a priority, it's just a wish.

6. It Reduces Financial Stress in a Very Real Way

Much of the money stress isn't really about not having enough money, it's about not knowing if you have enough money. If you don’t have a plan for your money, every unexpected bill is a crisis because you have no visibility into whether you can absorb it or not. Zero-based budgeting eliminates that uncertainty entirely. At any point of the month you can open your budget and see exactly what is allocated, what is spent and what is left. That transparency transforms money anxiety into money awareness. You may have no more money. But you will have total clarity on the money you do have.

7. It Builds Financial Discipline That Carries Into Everything

The discipline of zero-based budgeting is not in the spreadsheet. When you get in the habit of asking, “does this deserve a place in my budget?” each month, that question starts to show up in real time before purchases, too. Those who practice zero-based budgeting say it does change the way you think about money over time. It’s about awareness, not restriction. You stop spending mindlessly because you stop mindlessly thinking about money. That shift compounds like interest does.

How to Build a Zero-Based Budget in 5 Steps

You do not need any special tool or app to start. A pen, a piece of paper, and 30 minutes is genuinely all you need.

- Step 1: Write down your total expected income for the month. Include your salary, any side income, freelance payments, and anything else you realistically expect to receive. This number is your starting point.

- Step 2: List all your fixed expenses first. Rent or mortgage, loan repayments, insurance premiums, subscriptions, internet anything that does not change month to month. These are non-negotiable and go in first.

- Step 3: List all your variable expenses next. Food, transport, clothing, entertainment, eating out, personal care. These shift month to month so estimate honestly based on what you genuinely need, not what you spent last month.

- Step 4: Add savings and investment goals as dedicated line items. This is critical. Savings are not what is left over they get budgeted before you allocate to wants. Emergency fund, investment contributions, and savings goals all belong here.

- Step 5: Subtract everything from your income until you reach zero. If money is left over, assign it to savings or extra debt repayment. If you are over budget, reduce variable expenses until the numbers balance.

A Real Example: Zero-Based Budget on $3,000 Per Month

Here is what a practical zero-based budget actually looks like for someone bringing home $3,000 per month. These numbers are illustrative but realistic:

| Category | Amount (USD) | Notes |

|---|---|---|

| Rent | $900 | Fixed — 30% of income |

| Food and groceries | $350 | Cooking at home most days |

| Transport | $200 | Fuel or public transport |

| Utilities and phone | $150 | Electricity, water, internet, phone |

| Emergency savings | $300 | Building a 3-month buffer |

| Investment contribution | $200 | Index fund or savings account |

| Debt repayment (extra) | $200 | Above minimum payments |

| Clothing and personal care | $100 | Essentials only |

| Entertainment and dining out | $150 | Capped and intentional |

| Subscriptions | $50 | Only ones actively used |

| Miscellaneous buffer | $100 | Small unexpected costs |

| Medical / health | $100 | Co-pays and over-the-counter |

| Sinking fund (irregular costs) | $200 | Car service, gifts, annual fees |

| TOTAL | $3,000 | Every dollar accounted for |

Look for where savings and investments sit in that budget above entertainment, above subscriptions, above everything discretionary. That $500 going to savings and investments every single month becomes $6,000 in a year before any returns or compounding. At a modest 7% annual return over ten years, that habit turns into something genuinely significant. That is zero-based budgeting doing exactly what it is designed to do.

Who Should Use Zero-Based Budgeting?

Zero-based budgeting works best for people who are getting serious about money for the first time and want full control, anyone trying to clear debt aggressively and needs to find every spare dollar, people with irregular or variable income like freelancers and business owners, anyone who has tried other budgeting methods and found them too vague to be useful, and people who feel like their money disappears without explanation every month.

It is not necessarily the best fit for people who already have excellent spending habits and just want a light system to maintain them. For those people, the 50/30/20 rule or a simple spending tracker might be less demanding and still effective. But if you feel disconnected from where your money goes — zero-based budgeting will solve that problem directly.

The Honest Drawbacks You Should Know

It takes more time than other methods. Setting up a proper zero-based budget at the start of each month takes 30 to 60 minutes. For people with very simple finances this can feel like overkill. It also requires you to revisit your budget mid-month when reality diverges from the plan — an unexpected car repair, a medical bill, a last-minute flight. When something unplanned comes up, you have to redistribute from somewhere else, which takes attention and honest decision-making.

The first month is almost always uncomfortable. When you first build a zero-based budget you are likely to come face to face with a gap between what you thought you were spending and what you were actually spending. Most people find that confrontation difficult. But that discomfort is precisely the point. It is the feeling of awareness kicking in. It passes within two to three months once the habit settles, and what replaces it is confidence.

Tools You Can Use to Run Your Zero-Based Budget

You do not need to spend anything to start. A plain notebook and pen remains the most reliable budgeting tool in existence write your income at the top, list every allocation below it, subtract to zero. Google Sheets or Microsoft Excel work brilliantly too. Build a simple table once and reuse it every month. If you prefer a dedicated app, EveryDollar is a free web and mobile app built specifically for zero-based budgeting and works well for real-time tracking. YNAB You Need A Budget is the most powerful dedicated option available. It has a learning curve but once you get it, it is exceptional. It costs around $14 per month or $99 per year but comes with a 34-day free trial.

more budgeting type you may like:

- smar budgeting hack

- Zero-Based Budgeting (ZBB): The Complete International Guide to Mastering Your Money

- four walls budget

Frequently Asked Questions

What is the main benefit of zero-based budgeting?

The main benefit is complete visibility and control over your money. Every dollar is assigned a specific purpose before you spend it, which eliminates mindless spending, ensures savings happen first, and directly aligns your spending with your actual financial goals rather than leaving it to chance.

Is zero-based budgeting good for people on a low income?

Yes it is especially powerful on lower or irregular incomes. Because you start fresh every month based only on what you actually have coming in, the budget adjusts automatically to your reality. It helps you get the most out of every dollar even when there is not a lot of them.

How long does it take to do a zero-based budget each month?

Most people spend 30 to 60 minutes building their zero-based budget at the start of each month. After that, quick check-ins of 5 to 10 minutes throughout the month are enough to stay on track. It gets significantly faster after the first two or three months once the structure is familiar.

What is the difference between zero-based budgeting and the 50/30/20 rule?

The 50/30/20 rule works with broad percentage buckets 50% for needs, 30% for wants, 20% for savings and is more flexible but less precise. Zero-based budgeting assigns every individual dollar to a specific named category, giving you far more control and visibility. ZBB requires more effort but catches waste that the 50/30/20 rule typically misses.

Can I use zero-based budgeting if my income changes every month?

Absolutely it is one of the best systems for variable income. Because you restart from zero every month using only the income you actually received or expect to receive, the budget adapts automatically. Freelancers, contractors, and business owners benefit from this flexibility enormously.

What do I do if I overspend in one category?

You move money from another category to cover it. That trade-off is exactly the discipline the method builds. If you overspend on food, you reduce entertainment or miscellaneous to compensate. Every overspend becomes visible and deliberate rather than accidental, which over time makes overspending much rarer.

Do I need a special app to do zero-based budgeting?

No. A notebook and pen is enough to run a zero-based budget effectively, and plenty of people prefer it that way. Google Sheets works well too. If you want a dedicated app, EveryDollar is free and purpose-built for ZBB. YNAB is the most powerful paid option available at around $14 per month.

Zero-based budgeting doesn’t feel restrictive. This isn’t about living without fun. It’s not micromanaging every dollar spent on chocolate bars and lattes. ZBB is about being intentional with your money. When every dollar has a job you will stop questioning where your money went each month. Instead, you’ll be deciding where every dollar goes. Progress is made when you move from reactive to proactive with your finances. You don’t need to make six figures to start zero-based budgeting. You simply need to know your income amount, grab some paper, and spend 30 minutes at the beginning of the month. Seriously, that is all it takes. The compound growth of that small action each month will change everything.